iPhone sales are down, but ignore Apple’s shock result

April 27, 2016

April 27, 2016

Associate Editor, Digital

COMMENT

Apple, the world’s most valuable company, reported a quarterly profit of $US10.5 billion ($14 billion) this morning, and it was nowhere near good enough. Not even close.

Think about that for a second. This quarterly profit (nearly double the annual profit by Australia’s biggest company last year, the Commonwealth Bank), worked out to $US1.90 per share, but it was weaker than Wall Street had expected ($US2 per share). Apple stock has tumbled by 8 per cent in after hours trading in the US, wiping tens of billions of dollars from its market value.

The further you drill down into the result, the worse it looks.

People are turning their backs on Apple. Photo: Ben Rushton

As many analysts predicted, iPhone shipments (51.2 million during the quarter) declined compared to a year ago, the first time that has happened since the iconic handset was released back in 2007. The company’s total quarterly revenue shrank compared to the year ago period for the first time since 2003. And in China, an increasingly important market for the company and one of the key drivers of its growth, the tech giant was hit particularly hard, with revenue falling by 26 per cent.

Cue lots of talk about “peak iPhone”. Get ready for lots of thinkpieces about how Apple has run out of ideas, and how its new products like the Apple Watch just aren’t interesting. That it desperately needs a new hit to replace the iPhone.

All of which might be true.

But there are still reasons to think everyone should just calm down.

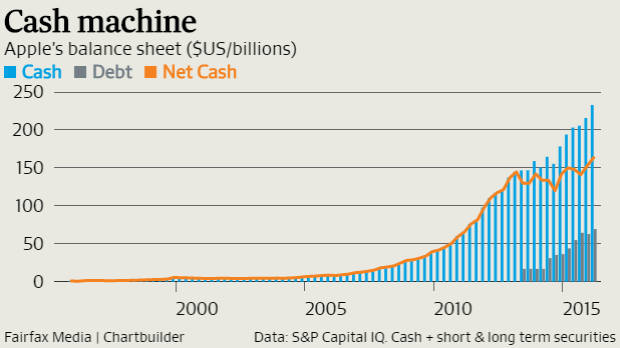

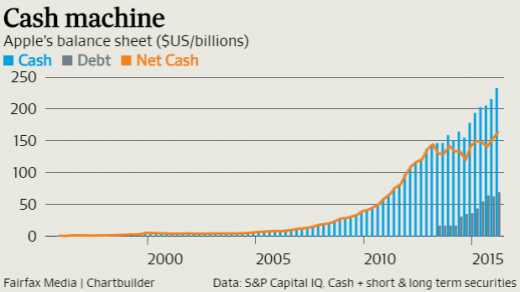

For example the company has a gigantic cash pile, which increased during the quarter and now stands at a truly ridiculous $US164 billion once debt is stripped out.

It’s not just the iPhone that is causing Apple headaches. Sentiment globally has turned sharply against corporate tax avoidance in recent weeks. Apple, which has consistently and vehemently denied any wrong doing, has long been criticised in some quarters for the elaborate steps it has taken to minimize its tax.

Yet for some investors, times like these, when sentiment has soured, provide the perfect moment to consider being brave and buying stock.

“While the headlines of declining iPhone shipments and revenues appear scary, we think this is largely the result of the company being in between product cycles,” says Andrew Macken, a portfolio manager at Montaka Global, which holds Apple shares. “At a price-to-earnings ratio of less than eight times, we think Apple offers attractive value at its current share price.”

Brandon Geisler, of Denver-based asset manager Marsico Capital, said the result confirmed his concerns that the smartphone market is now saturated. Geisler, who doesn’t own Apple shares for his fund, says most of the innovation going forward will be in software, rather than in hardware, so he is investing in the likes of Facebook and Amazon.

But even he acknowledges Apple still has plenty of promise. “Apple remains an exceptionally well run company that generates significant amount of cash for shareholders,” he says. “The long-term success of the company will hinge on the development and adoption of new software and services to monetise their global ecosystem.”

The growth for the iPhone may well be over, and Apple might never develop a product as successful as the handset. But it also has a gigantic cash war chest to at least try and find one. Not to mention a massive base of customers, who will likely keep upgrading their devices every couple of years, and to whom it can sell other stuff, like software. Apple said on its earnings call that it estimates the size of its “installed base” of active devices to be more than 1 billion.

As Tim Cook said on the call: “Those 1 billion-plus active devices are a source of recurring revenue that is growing independent of the unit shipments we report every three month”.

Think iTunes and the App store, its payments apps, and so forth. Services revenue actually increased by 20 per cent to $US6 billion, and it was the company’s second biggest revenue generating business, Apple said, bigger than revenue generated from sales of Mac computers and the iPad.

To be sure, Apple’s software products have been shoddy in the past (Apple Maps and Music spring to mind) but it’s clear that’s where the company sees an opportunity going forward.

And remember, Apple’s war chest is so big it can experiment with cars, or virtual reality, and still have more than enough left to shower its shareholders with dividends (it actually raised its dividend again during the quarter) and buy back stock to bolster the share price.

Yes, Silicon Valley, and aspects of the US equity markets, are obsessed with growth and don’t cope well with maturing companies.

Apple may or may not have reached that point. But regardless, it still has a hell of a lot going for it, as both a company, and an investment.

The iPhone boom may be over – but never underestimate Apple and its gigantic war chest to find the next big thing.

(12)