The Fight For The $400 Billion Business Of Immigrants Sending Money Home

“Dollars wrapped with love.” That’s how Dilip Ratha describes remittances—the money immigrants send home to their families and friends. “There are millions of people who migrate each year. With the help of the family, they cross oceans, they cross deserts, they cross rivers, they cross mountains,” Ratha, an economist, said in a 2014 TED talk. “They risk their lives to realize a dream, and that dream is as simple as having a decent job somewhere so they can send money home and help the family, which has helped them before.”

For a long time, economists tended to overlook these dollars, but recently they’ve come to appreciate their importance. Remittances, which totaled $ 429 billion in 2016, are worth three times as much as all the foreign aid doled out by governments worldwide, and it’s likely the money is more effective dollar-for-dollar. Unlike aid, which is notorious for passing through corrupt middlemen and inefficient bureaucracies, remittances go directly to recipients, where they pay for schooling, medical expenses, and new fridge-freezers. In some poor countries, like Somalia or Haiti, remittances make up more than a quarter of national income. And statistics show that remittances tend to hold up even in times of crisis. After the financial crash of 2007-2008, the intra-family flows continued even as private capital ground to a halt.

But that’s not to say that remittances couldn’t be more effective. New startups are aiming to do for international payments what Venmo and others have done for domestic transactions: make transfers mobile, painless, and social. “In 5 years or 10 years, the whole idea of a remittance or cross-border payments will be gone, just like we don’t have cross-border email, or cross-border web browsing. It’s just the internet,” says Jeremy Allaire, CEO and founder of Circle, a blockchain-based service that’s working on the remittance market.

Currently, it’s expensive to send money overseas, which is especially damaging for the immigrants sending small savings home to the developing world. The World Bank says transaction fees average 7.45% globally, and, in many remittance corridors, they’re a lot higher than that. Sending money to Africa from the U.S. or Europe sometimes costs an extra 15%, and within Africa, the fees can be stupendous. To transfer 33,000 Angola Kwanza (about $ 200) from Luanda to Namibia costs about $ 50, according to the World Bank’s price database.

But in the last 10 years the average global fees have fallen by about 2.5%, which equates to about $ 90 billion in extra love-dollars, the World Bank’s Marco Nicoli says. The D.C. institution works to bring more transparency to remittance pricing (the database lets you compare providers), and it lends money to poorer countries to beef up their payment systems. A further 5% drop in fees would mean $ 16 billion in extra annual income for recipients, it says.

In his speech, Ratha suggests several reforms, including loosening money laundering regulations on amounts lower than $ 1,000, ending monopoly arrangements between post offices (which often disburse remittances) and money transfer companies, and creating a new low-cost remittance system funded by philanthropy. But new technology and the boldness of an emerging group of money transfer startups–like Circle, and others like Abra, Transferwise, and WorldRemit–could also have a profound impact. The combination of the internet, mobile phones, bitcoin, and the blockchain could dramatically reduce the cost of sending money internationally, say experts. That is, if the startups are allowed to grow unimpeded by unnecessary regulation and special interest griping, including from banks and exchange companies that currently gain handsomely from the fees and inefficiency in the space.

The High Costs Of Sending Cash

There are several reasons why the cost of sending money cross-border is currently so high. Nicoli notes that most payments start and finish as cash, which means that human agents need to be employed to receive and disburse the money, raising the price for everyone.

Bill Barhydt, founder and CEO of Abra, points to all the “hands in the pie” in traditional transactions, like those orchestrated by market leaders like Western Union, MoneyGram, and RIA. Remittances can be initiated via an agent (like those affiliated with Western Union or MoneyGram), a bank branch, a post office, the internet, and via mobile. So there’s someone at the cash window taking the money. There’s the agent’s bank. There are “correspondent banks” on both sides of a national border. There’s the bank for the agent in the receiving country. There’s the disbursing agent. There’s Western Union or MoneyGram itself.

Founded in 1851 as a telegraph company, Western Union has more than 550,000 agents in 200 countries. It completed 268 million consumer transactions in 2016, worth $ 80 billion. Together with MoneyGram and RIA, it controls more than a quarter of the international market. And, as its longevity implies, it’s been adept at beating back competition before now. The company generated revenue of $ 5.4 billion in 2016, with operating income of $ 484 million.

In an interview with Fast Company, Western Union’s chief information officer David Thompson says the cost of regulatory compliance, including new anti-money laundering regulations introduced after 9/11, raises the cost of sending money internationally. (Banks and transfer companies are now required to identify customers and report transactions in excess of $ 10,000). But the compliance burden also makes it difficult for new entrants to eat into its business.

“Western Union is in a highly regulated industry globally, requiring licenses in every jurisdiction you operate in. You need a strong money laundering and broad risk program in place,” Thompson says. “Technology doesn’t solve all those business and regulatory issues. Some pure technology plays forget that. We live in a world with criminal networks and entities that you have to keep out of your infrastructure. There’s a pretty high barrier to entry because of the risks associated with the market.”

In his TED talk, Ratha has a less complicated explanation for the high cost of remittances. “Money transfer companies structure their fees to milk the poor,” he says. Development groups often point to a lack of competition and financial regulation in poorer countries. African migrants in particular pay a so-called “super-tax” on international transfers, and the market power of MoneyGram and Western Union is likely one proximate cause. In a 2014 report, the London-based Overseas Development Institute said the “two companies account for $ 586 million of the loss associated with the remittance ‘super tax,’ part of it through opaque foreign currency charges.” Ratha says governments should require higher standards of transparency from money transfer companies on exchange rates, and the fees and taxes they charge both senders and recipients, so it’s easier for immigrants to shop around. Some smaller exchange providers even charge fees to people collecting remittances, further inflating costs, he says.

The Disruptors

The good news is that a string of competitors are now appearing, aiming to cut prices and improve transparency. London-based WorldRemit calls itself the “WhatsApp of Money.” Started by Ismail Ahmed, a Somali-born former United Nations official, it facilitates mobile money (or airtime) transfers to more than 140 destinations and now does 580,000 transfers every month. The London startup has received more than $ 150 million in venture capital from investors who backed Facebook, Spotify, Netflix, and Slack. Ahmed’s seed money actually came via the UN in the form of compensation for wrongful workplace treatment. He had alleged corruption in the UN’s development program in Somalia and faced retaliation (a potential employer was told not to hire him) after making his claims public.

TransferWise, set up by two former Skype employees, tries to bypass bank wire fees. It pairs up people needing to send money in different directions, so the money never needs to go cross-border. So, if you want to send $ 100 from the U.S. to Germany, you put the money in the company’s U.S. account. TransferWise then finds someone who wants to send money from Germany to the U.S. and that person pays their money into its German account. Instead of either side paying a hefty wire transfer fee, the transfer is made domestically, with TransferWise covering the balance. The idea has been called “Hawala with paperwork” after the traditional Islamic banking system whereby value moves around an international network of brokers without physical money ever actually being transferred. TransferWise charges 1% of the transfer amount up to $ 5,000, with no additional charges hidden in the exchange rate conversion (Banks, it says, will often exchange your money at less than the official rate, pocketing the difference on top of a fee).

Another company, TransferWise, which has Peter Thiel and Richard Branson as investors, recently announced that it’s integrating with Facebook’s Messenger Chat service, as are a host of other major players, including PayPal, MasterCard, American Express, and Western Union. The latter also has mobile partnerships with Viber and WeChat (though this hasn’t stopped criticism that it obfuscates pricing through a mixture of fees and exchange rate mystery).

The promise of bitcoin and blockchain-based startups is that they dis-intermediate corresponding banks from the settlement process. Remittances have traditionally been settled using wire or SWIFT–transfers within a network of international banks. But they don’t allow small payments of $ 5 or $ 10, and, because of fixed fees, they’re relatively expensive for amounts of, say, $ 200 or $ 500, say remittance experts. Many new startups (though not TransferWise) offer greater convenience at either end of the transfer (the money appears on your phone’s wallet or in your online bank account). But they still go through the traditional banking system, so their potential in lowering costs is limited.

“We have seen more innovation in the delivery channel stage of the transaction where players allow transactions to be initiated over the internet in different forms,” says Nicoli at the World Bank. “Ultimately, however, most of these models have to rely on the corresponding banking network. This is where where the potential of [distributed ledger technology] and blockchain innovation is.”

Though bitcoin itself has a sometimes unsavory reputation, the distributed ledger technology underlying bitcoin is now being developed as a settlement engine for all kinds of financial products, from stocks and bonds to loyalty points and insurance contracts. Blockchains–ledgers running simultaneously on millions of devices–offer cheaper, more secure record-keeping than the banking system. And, they can be used to transfer virtual currencies (like bitcoin) as proxies for traditional currency exchanges. Thus, they have potential to dramatically reduce costs.

“As blockchain technology matures, it has true disruptive potential to bring the cost of remittances to nearly zero and facilitate instant secure payments anywhere in the world,” writes Talie Baker in an Aite Group report about emerging remittance startups.

Abracadabra

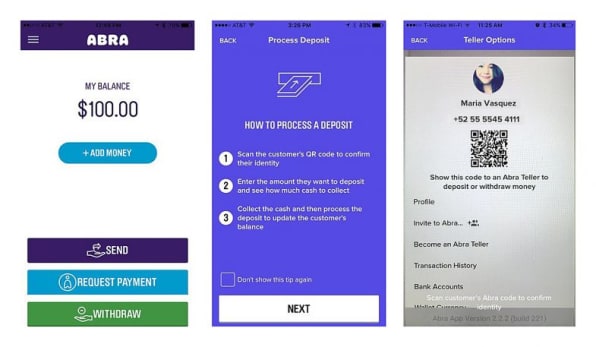

Abra, which says it can reduce transaction costs by up to 90%, has an ingenious way around the international settlements system. It uses bitcoin to transfer value instead. You load money from a bank account or human “teller,” to a mobile phone wallet. Abra converts the money into bitcoin, transfers it across the digital currency’s blockchain, then settles the amount in a local currency on the other end.

Importantly, customers never know they’ve just undergone a bitcoin transaction: Abra’s app looks and feels like any one of dozens of money transfer apps (like Venmo). And Abra also offers a service for people who don’t have bank accounts. It signs up “tellers” in different countries who, like Uber drivers, act as “human ATMs” on its behalf. Using the app, you find someone nearby willing to convert your cash to bitcoin. You meet up, hand over what you want to send via Abra, and the teller takes a small fee for offering the service (they set the rate themselves). In such a way, Abra hopes to build out an extensive network of agents, but without making a hefty investment in infrastructure.

Having launched in 2016 in the U.S.-Philippines corridor, in March the company expanded to 155 countries and now accepts and disburses money in 54 local currencies. Abra, which has received capital from American Express Ventures and other high-profile VCs, charges no fees for transferring money (though you need to pay your teller if you don’t want to use the bank account method). It makes money on the exchange rate, though it claims to offer better prices than Western Union.

Barhydt says Abra has tellers in 150 cities so far. Each has to undergo a one-to-one interview to ensure suitability. Most are already trading in bitcoin either independently or via a digital currency exchange (like Kraken).

Unlike other remittance startups, Abra doesn’t have banking licenses in all its locations, instead classifying itself as “non-custodial” and therefore exempt from regulations. Circle, on the other hand, uses bitcoin for transfers but takes possession of funds during transfers. It’s focused less on unbanked consumers and remittances, though that’s also part of its target business.

As Baker says in her report, using bitcoin is not without risks, because bitcoin’s legality is still questioned in some places. “Bitcoin is still an experimental currency in active development, and nobody can predict its staying power. It is not an official currency, and some jurisdictions even consider it illegal,” she notes (though Baker is excited by Abra and Circle, describing them in an email as “viable business models” with the potential to give Western Union and MoneyGram “a run for the money.”)

Allaire, at Circle, expects the exoticness of blockchain and bitcoin to retreat into the background as the technologies gain wider acceptance, including for remittance payments. “Consumers don’t care about the name of the technology. They want services that let them do things faster and cheaper,” he says. Backed by Goldman Sachs, Circle is already transacting more than $ 1 billion a year.

Western Union is still working out its approach to blockchain and bitcoin. It has invested in Digital Currency Group, a major fund for such startups, and last year it ran a small pilot program with Ripple, a payment protocol provider. But Thompson says the trial didn’t deliver “significant business value” or “return sufficient value for our shareholders,” and the idea isn’t being pursued.

For the moment, Western Union isn’t prepared to tear up its existing business, even as it migrates to mobile and Facebook Messenger. “We feel that the investment we’ve made in our infrastructure, our team, our processes and policies are our secret sauce, and that’s why Western Union has been in business for 165 years,” Thompson says.

Maybe so. But, with all the startups gunning for its business, Western Union is going to have to work harder than ever to maintain its position. The next few years will dictate if Western Union can last another 165 years or whether its high-fee model–one that appears injurious to many immigrants around the world–can survive in its current form.

(40)