the typical American has a number of debt: $15,355 in bank card debt, $26,530 in auto loans, and a personal loan of $a hundred sixty five,892, in step with the financial website online NerdWallet. and those that lift student loans have a regular balance of $forty seven,712. All of this debt prices the typical household $6,658 in pastime each 12 months, which is 9% of the average household earnings.

That’s some huge cash going out the door, and i used to know exactly what that felt like. 4 years in the past, my husband and that i were $200,000 in debt, with $25,000 on credit cards, $21,000 in auto loans, and a personal loan of $154,000. however on October 16, 2015, we wrote a take a look at for $6,292, the steadiness of our mortgage and our final remaining mortgage, and became officially a hundred% debt-free. We joined a minority of americans—about 20%—who don’t owe somebody anything. it’s an unique club, but there’s hope that it’s growing. About half of american citizens point out that being debt-free is inside attain, and 25% say it’s the brand new American Dream, consistent with a credit score.com survey.

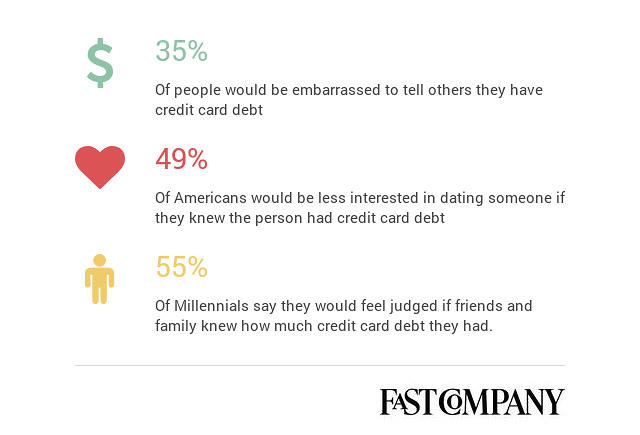

With the great Recession now in our rearview replicate, many of us believe debt to be a kind of four-letter phrases. Blame aside, it got us into the up to date monetary battle, and our attitudes about borrowing are changing. A up to date poll carried out by using NerdWallet discovered that 35% of individuals can be embarrassed to inform others they have bank card debt, and 49% of americans would be less all in favour of dating any individual in the event that they knew the individual had bank card debt. Millennials are especially delicate about debt: fifty five% say they might really feel judged if friends and family knew how much bank card debt they had.

“Many millennials came of age all the way through the recession, which could explain their fear of credit cards and the potential debt that comes along with using them incorrectly,” says Sean McQuay, NerdWallet’s in-house bank cards professional. “as a result of this bias, it makes sense that millennials see credit card debt as one thing that should be judged.”

What separates the individuals who will cross the debt-free finish line from people who never will is a willingness to acknowledge how a lot debt you have, says A.J. Marsden, assistant professor of human products and services and psychology at Beacon school. “a lot of people are in denial, refusing to look closely at their own funds,” she says. “They don’t need to provide you with a financial plan, in order that they proceed to buy with out thinking.”

consumers, actually, vastly underestimate how much debt they have got. consistent with NerdWallet, lender-said credit card debt used to be one hundred fifty five% larger than borrower-mentioned balances in 2013.

For my family, our financial warning sign came in 2008 when the auto industry’s outlook was once lovely dangerous, and we have been concerned that my husband’s job would depart. We had all the time talked about being debt-free, but by no means actually put our cash the place our mouths had been. The shaky economy had us rethinking purchases, canceling holidays, selling stuff on eBay, and making a finances for the first time. Two years in the past, when the automobile coast looked clear, we noticed the light on the end of the tunnel and bought “gazelle extreme,” as financial writer Dave Ramsey would say. We listed our last debts on a whiteboard that we hung in our kitchen and knocked them out one by one. The personal loan was once the remaining to fall, and we obtained there via following the debt-snowball advice of Ramsey, the computerized payments and financial savings recommendation from Ramit Sethi, creator of i’ll train You to Be wealthy, and the badass suggestion from early-retirement guru Mr. money Mustache.

while we plan to by no means go back, a manageable level of debt approach your shopper debt payments aren’t more than 10% of your monthly profits, says Marsden. “unfortunately, it’s no longer exotic to look people with shopper money owed at 50% to eighty% of their month-to-month earnings,” she says. And when the debt ratio starts creeping up, so do psychological and bodily unintended effects.

Debt And psychological health

individuals who fight to repay their money owed are more than twice as likely to undergo from psychological health concerns together with anxiousness and depression, in keeping with a find out about from the college of Nottingham published within the economic Journal. in addition they really feel constantly beneath pressure, hopeless, and incapable of determination making.

“One putting discovering of my research is that many people with debt problems describe emotions of being unable to be aware of day-to-day actions or make customary selections. This has wider results on their attitudes and basic health,” writes lead researcher John Gathergood.

Debt And physical well being

a rise in debt additionally brings a rise in stress that may take place itself physically, says Marsden.

“Stress performs a big position in heart disease, and there is a important sure correlation between debt and coronary heart attacks,” she says. “The extra debt you could have, the larger your chances of having a coronary heart assault from the stress.”

Stress additionally brings conditions similar to migraines, weight problems, and accelerated growing older. ironically, many people practice “retail therapy” to counteract the stress, however that simply adds more gas to the hearth.

limited selections

Having debt affects what a person can and can not do, says Coleen Pantalone, a finance professor on the D’Amore McKim school of industry at Northeastern university.

“Carrying an excessive amount of debt limits option, on occasion self-imposed and now and again imposed by means of a poor credit, leading to lenders refusing to lend more,” she says. “We steadily hear nowadays about the issue in saving the down payment for a first home for the reason that person has scholar debt, along with perhaps a automotive loan or rent and bank card debt.”

Debt additionally impacts your alternatives, says Pantalone. “for instance, it’s dangerous to alter jobs or careers in case you have all these fixed funds due every month,” she says. “Debt can restrict your attainable and your own smartly–being.”

Resentment

whenever you well known your debt, the reality can lead to you to have anger towards your companion or your self, says Marsden. “you could ask, ‘How did I/you let it get his unhealthy?’” she says.

you may also resent your agency if you are feeling you aren’t paid sufficient, family members who’re based upon you, or your folks for no longer instructing you better financial lessons. And debt is harmful to your relationships, particularly your marriage.

“Arguments about money is via a ways the top predictor of divorce,” writes Sonya Britt, assistant professor of family studies and human services and software director of private financial planning at Kansas State university. “it is no longer kids, intercourse, in-regulations, or the rest. it is money—for each men and women.”

hazardous habits

Debt is a taboo subject: americans would relatively talk about religion or politics than money, according to the NerdWallet learn about. This fear can lead anyone to make bad alternatives, reminiscent of going out to a luxurious dinner or replacing dear presents, with a view to keep up appearances with domestic and chums as an alternative of being trustworthy about their struggle with debt.

And a large amount of debt can lead anyone into unsafe behavior, comparable to opening some other bank card, taking over a high pastime mortgage, or getting a second mortgage, says Marsden.

What It Feels prefer to Be Debt-Free

Paying off your debt is quite releasing. It eliminates all of the issues and unwanted side effects that debt can bring. And it offers you a sense of security that comes with the truth that you don’t owe anyone anything; your selections will also be totally your personal. for my part, I not wring my hands over late tests that can be common while you’re a freelancer. And my husband doesn’t have to stress over the health of his business, because we aren’t depending on maintaining a definite income level.

“When people pay off debt, they’re going to say, ‘My stomach feels better, my heart feels better,'” Washington psychologist Carole Stovall advised Fox trade. “a wedding that survived the problem—without the casualties of lost recognize or bitterness—will possible develop better, and that completely has a trickle-down impact on children.”

Your first step is recognizing the problem and growing a plan. “Debt is beginning to develop into a worse drawback than it used to be in the past, as a result of it’s so easy to click on and purchase,” says Marsden. “the hardest section is sticking to a price range.”

but imagine me—it’s value it.

quick company , read Full Story

(66)