One hundred and sixty-eight years ago, at a time when U.S. states still minted their own currency and the Statue of Liberty had yet to be built, a Bavarian immigrant by the name of Marcus Goldman first stepped foot on American soil. For two decades our humble hero made a living as a peddler and shopkeeper. Then, in 1869, he reinvented himself as a banker, brokering IOUs from a basement office next to a coal chute in the shadow of Wall Street. He died at age 82, father to five children and the beginnings of a financial empire.

Chances are you’d be happy to borrow money to pay off your debt from a hardworking family man like Marcus, his success story writ in sepia tones. Or that at least is the theory behind Marcus by Goldman Sachs, the lending product for everyday Americans that the Wall Street firm unveiled today, more than a year after installing Discover executive Harit Talwar at the product’s helm. Marcus lives online, powered by a custom-built technology stack, but traffics in nostalgia, with old-fashioned typefaces and illustrations. Visiting the Marcus home page feels a bit like posing in the “old time” photo booth at an amusement park, your hoodie and jeans hidden behind a dapper three-piece suit with cravat.

The sense of history is very much by design. Marcus joins a crowded field of online lending startups, all chasing after a U.S. market worth as much as $1 trillion, excluding mortgages. But none benefit from the direct backing of a parent institution like Goldman Sachs, with its longevity and balance-sheet billions. As an extension of GS Bank USA, Marcus can fund unsecured personal loans without simultaneously having to find investors willing to buy them. For consumers, that arrangement translates into more flexible loan terms and an interest-based business model that eliminates the need for fees—if, of course, potential borrowers can stomach the idea of doing business with a financial institution that many labeled a pariah during the financial crisis.

“We were eyes-wide-open to the attending challenges,” Stephen Scherr, chief strategy officer for Goldman Sachs and CEO of GS Bank USA, says of the process that led the bank to commit to launching a consumer-facing product. Scherr has helped shepherd Marcus from its earliest days as part of a task force of five senior leaders evaluating growth opportunities. “We would be facing off against a different customer set. We would be subjecting ourselves to a wider scope of regulation. We would be opening the franchise and the brand to something that it had not been open to before. But at every one of those forks in the road, we always came to: ‘Do it.’”

Should have left a voicemail

To some extent, all the big banks became the target of public anger in 2008 for enriching themselves while leveraging the financial system to a point of near-collapse. In the Great Recession that followed, millions lost their homes and millions more watched, helpless, as portions of their retirement savings evaporated. The hostility directed at Goldman Sachs has been particularly intense, with Matt Taibbi’s condemnation of the bank for being “a great vampire squid wrapped around the face of humanity” becoming an era-defining viral sound bite.

But the bank’s great sin was not its ability to make money (though the power of its profit-machine certainly generated envy—and some resentment—among its peers). Instead, it was that Goldman Sachs lost sight of its focus on serving clients. “Long-term greed,” a principle the firm enshrined in the 1950s, had given way to a culture that could accommodate hot-shot millionaires brazenly celebrating “shitty deals” over email at clients’ expense as they floated in pools of bonuses in loosened Hermès ties.

“The whole building is about to collapse anytime now . . . only potential survivor, the fabulous Fab,” Goldman vice president Fabrice Tourre, who was later found guilty of securities fraud, wrote in a 2007 email to a friend—hardly an example of “client first” service.

“What really snapped my head back were the callous emails,” CEO Lloyd Blankfein says in an internal company video, from 2011. “When people are telling us we’re too clever, and we’re saying we’re not in the wrong and that clients come first . . . and then we go out and confirm their thoughts with emails like that—you have to remember the firm only has one reputation. If you have a problem in one space, it affects us all.”

At the time of the crisis, Goldman’s clients were corporations, hedge funds, and fellow banks, plus a select group of high-net worth individuals. While Congress and the broader public were railing against Goldman for its staggering bonuses (in 2009, the average employee made $498,000, even after the firm set aside $500 million from its bonus pool to donate to charity), those wholesale clients were beginning to question the firm’s conflicts of interest. Sometimes Goldman was making bets with client money, and sometimes with money of its own: Where did its loyalties lie? In 2010, a client survey conducted by the Boston Consulting Group revealed widespread “trust issues with Goldman as a whole,” according to an executive quoted in the resulting Harvard Business School case study. The survey dumped cold water on the idea of Goldman, Sachs & Co. as Wall Street’s patrician fortress; somewhere along the way, that proud history had become a myth.

Internal reforms have to some extent appeased the bank’s traditional client base. But the long shadow cast by public anger continues to haunt Goldman Sachs’s reputation, undermining its ability to attract talent and fuel growth.

Marcus: “On your side”

With Marcus, its first consumer product, Goldman has a shot at redemption—and an opportunity to leverage the influx of deposits on its balance sheet, added in response to post-crisis capital requirements that reflect its new identity as a bank holding company. The institution hired Talwar, a Goldman outsider and consumer banking veteran, to lead the startup business unit, then code-named “Mosaic,” in May of last year. Under his watch, Marcus has maintained its narrow focus on a particular subset of personal loans, one that is sure to placate regulators concerned about consumers’ financial health and rankle Goldman’s fee-hungry banking rivals: credit card debt consolidation, a market worth more than $450 billion.

“We are building a startup inside Goldman to help Americans manage debt better,” Talwar says. “To be able to do that well, we have kept the customer at the center of everything that we do.”

The fixed-rate, no-fee loans will range from $3,500 to $30,000, to be paid back within two and six years. Talwar plans to target borrowers with decent credit but ballooning debt, a task that requires destigmatizing a delicate topic. Marcus’s marketing materials are direct, but encouraging: “Debt happens. It’s how you get out that counts.” APRs will range from 5.99% to 22.99%, with an expected median in the 12% to 13% range.

At Marcus’s offices, located on the 26th floor of Goldman Sachs’s lower Manhattan headquarters, there are numerous reminders of that customer-centric mission and the flat management structure that Talwar prefers. Long walls of windows face north and east, punctuated by posters of example customer journeys and signs that reinforce the Marcus brand: “On your side,” they read, supported by brand pillars like “value” and “transparency.” In the northeast corner, with its sweeping views, there is not an executive office but rather a shared “living room,” complete with popcorn machine (“Goldman Snacks,” says the printout above).

The New York-based team, almost 200-strong, gathered here on a recent Wednesday morning for their weekly huddle, which provides an opportunity for cross-functional “squads” to report on progress. Talwar started making hires last July and initiated the first two-week product sprint last November. He glances at his Apple Watch and steps forward as the group quiets. In Salt Lake City, more than 60 customer service team members have joined via dial-in.

“Everyone, thank you,” Talwar says with a nod and a smile. His leadership posture is one of Yoda-esque understatement, with sloping shoulders, graying tufts of hair, and a habit of standing hands clasped, elbows close to his sides. “First of all, apologies for doing [the huddle] a little later today. We were upstairs with senior management doing a product demo and showing them the marketing materials. I want you all to know, they were feeling very good about what they saw.”

“No changes, right?” someone calls from the back of the room.

“No changes,” Talwar responds, joining the team laughter. Marcus may be a startup of sorts, but its leaders are well aware that their investors are just an elevator ride away. Talwar’s tone grows more serious: “But feeling good means that our burden of responsibility keeps increasing, correct? We’re going to need all your reservoir of stamina and energy moving forward.”

Launch is weeks away, after nearly a year of sprints. But the real work is just beginning.

Marketplace growing pains

Online lending has exploded over the last few years, thanks in part to a low-interest rate environment that has been friendly to startups, who in turn have been friendly to lower-credit borrowers. With a few clicks, consumers can pay off their credit card debt, refinance their student loans, or cover their medical bills. In 2013, U.S. online lenders generated $4.4 billion in loan volume, according to a joint report published in April by the Cambridge Centre for Alternative Finance and the University of Chicago Booth School of Business. Last year, their total volume hit $36.2 billion.

Startups like Lending Club and Prosper have led the way, introducing consumers to this new type of credit in the form of personal loans. More recently, financial technology startups that initially focused on refinancing student loans, like CommonBond and SoFi, have added open-ended personal loans to their roster of products.

Marcus enters the fray at a time of reckoning for this still-nascent industry. In May, market leader Lending Club ousted its founder and CEO, Renaud Laplanche, after discovering that he had knowingly sold loans to an institutional investor that did not meet the investor’s explicit criteria. Lending Club’s stock plunged and Laplanche, once an industry hero, became a persona non grata (Goldman’s investment bank helped Laplanche take his company public in 2014).

More troubling, though, than the management malpractice at one company was the crack that Laplanche exposed in the marketplace model he had championed. With help from banks, marketplace lenders create tranches of loans and sell them to investors. Thus packaged, the loans become a security, like a stock or a bond, that investors can buy and sell. Marketplace lending is an attractive model for startups in that it enables them to quickly ramp up their loan volume. But it leaves the lending startups vulnerable, every quarter, if investors decide to walk.

“You can’t really stockpile funding to use for a rainy day,” says Jefferson Harralson, who covers Lending Club for Keefe, Bruyette & Woods.

Online marketplace lenders, the U.S. Department of the Treasury cautioned in a recent report, have not “yet been tested during a downturn in the credit cycle.” Treasury also questioned the “durability of technology-driven operations and credit underwriting” and the “sustainability of investor demand for loans.”

As a result, many startups are now keeping some loans on balance sheet or at the very least diversifying their funding sources. Most believe that the top players will pull through. “I don’t think there’s going to be a massive ongoing hangover from the Lending Club events, I just don’t,” says Sam Hodges, cofounder of small business lender Funding Circle USA, though he acknowledges that the fallout “slowed down” some investor conversations. But for marketplace lending’s minor league startup teams—there are more than 200 players in the U.S. alone—consolidation looms on the horizon.

Marcus, in contrast, relies on parent Goldman Sachs’s balance sheet, billions of dollars strong, to fund its loans. The benefits are significant, and Talwar plans to take advantage of them.

“Too many banks give customers a feeling that they don’t have options,” he says. The same is true of most marketplace lenders, in the sense that they slot customers into standardized loans that facilitate securitization. Marcus starts where customers are likely to start: with how much they can afford to pay per month. “‘I can pay $400. Now tell me what options there are,’” Talwar recalls hearing focus group participants say. Unlike its competitors, Marcus can turn that preference into a loan term of 31 months, for example, as opposed to 24 or 36 months. If taking out a marketplace loan is like buying a suit off the rack, taking out a balance sheet loan is like ordering a suit made to measure.

In theory, large banks like Bank of America and JPMorgan Chase could develop and fund a product like Marcus via their balance sheets, which dwarf Goldman’s in scale. But in practice, doing so would cannibalize their credit card businesses. (There is a chance that Goldman’s capital markets division might lose out on marketplace lending securitization deals as a result of Marcus, but Scherr says the product is unlikely to have a material impact on those relationships.)

Marcus’s personalized approach, says Talwar, is a result of being able to combine the best of online lending (modern technology) with the best of legacy banks (cheap funding, via balance sheet deposits). “That is what we mean when we say that our competitive advantage is [being a] startup with heritage.”

On Main Street, a friendly face

The product’s brand positioning—Marcus by Goldman Sachs—is designed to convey that duality.

“We learned that Goldman Sachs brought a lot of good equities to this consumer—things like being known for technology and financial expertise, and having this heritage for over 100 years,” Dustin Cohn, head of brand and marketing communications for Marcus, says of the research his team conducted. “At the same time we knew there was an opportunity to infuse a level of techie, Silicon Valley-type vibe, a freshness, a modernity that a brand like this would need to have.”

After choosing the brand’s “by Goldman Sachs” structure, Cohn and his team developed more than 2,000 possible names to place before the colon. “‘Marcus’ really came across as friendly and accessible and personal,” as opposed to names that contained words like “loan” or “digital” and were more “telegraphic,” Cohn says. Plus, he adds: “Down the road could we offer different kinds of loans, different kinds of financial services—it gives us that sort of runway,” all under the Marcus banner.

There is early evidence that Goldman-affiliated retail products can gain traction. The online deposit platform the firm acquired from GE, for example, has grown from $8.75 billion to $11.14 billion in savings deposits in the six months since the deal closed, thanks in large part to 43,000 new accounts. (Though it doesn’t hurt that GS Bank is paying depositors a premium interest rate, now at 1.05%.) Similarly, the active, quant-driven exchange traded funds (or ETFs) that the bank introduced last year have already attracted $2.4 billion in assets—three times the total of a similar product developed by JPMorgan, which had a year’s head start in the market.

Goldman has “a real panache” with registered investment advisers in small-town America, David Nadig, ETF director at FactSet Research Systems, told Bloomberg.

Brand cachet, of course, does not always translate into product quality. “We are looking forward to competing with Goldman Sachs on customer experience,” Scott Sanborn, then Lending Club’s chief operating officer, told the audience at an American Banker conference last fall. Now, as CEO, he’ll get his chance.

You’ve got mail

Customer experience in online lending is as much about what happens before you arrive on a landing page as it is about what happens once you get there. The most sophisticated lenders operate finely tuned funnels that take high-potential prospects from printed mailer or Google ad to cash in hand. To encourage prospective borrowers to complete their loan applications, lenders pre-fill forms and minimize the amount of information required to generate an offer.

“The holy grail is one field,” ideally an email address, says Peter Renton, founder of Lend Academy and the LendIt industry conference.

Marcus launches today with a direct mail campaign targeting prime borrowers carrying a revolving balance on their credit cards. Letters containing offer codes will go out to a few million homes, giving the team an opportunity to continue refining the product before making Marcus available to all, on a to-be-determined date. (In 2015, 13.7 million Americans took out an unsecured personal loan.) It may seem counterintuitive, but direct mail is generally considered the best way to reach pre-qualified prospects, because of the profile data available through credit agencies; industry-wide, online lenders source roughly half of their borrowers in this way.

Marcus’s direct mail collateral, printed in brand colors navy blue and salted caramel, does not shy away from competitive comparisons. In one example page, a table calls out Lending Club, Prosper, Wells Fargo, and Discover for their high APRs, late fees, payment date constraints, and more (Talwar was not involved in managing Discover’s personal loans). The table suggests that relative to other financial services companies, Marcus—and by extension, Goldman Sachs—doesn’t look so bad.

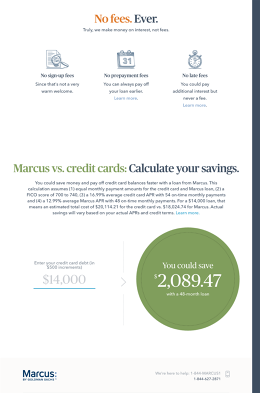

To cater to prospective customers who arrive via digital means the product team has developed two interactive tools. One takes direct aim at banks: “Marcus versus credit cards: Calculate your savings,” the site says. When visitors enter their anticipated loan amount, Marcus generates a savings estimate in a green bubble. In my product demo, taking out a Marcus loan for $18,000 led to $2,686.46 in savings.

The second tool is a pair of dollar-range “sliders,” which invite borrowers shopping for offers to experiment with loan amounts and monthly payments, a feature that echoes one that startup lender Earnest previously developed.

“When I arrived we had these grandiose ideas,” like clickable bars and charts, says Carl “Boe” Hartman, chief technology officer for Marcus. “It became very clear to us that we were over engineering that experience.” Hence the calculator and the sliders, both pared down to their simplest form: “You put in a number, you get a result.”

“There are no rainmakers”

Early on a September morning, with the product undergoing its final tests and launch day looming, Talwar and I meet for breakfast at Gee Whiz diner, a couple of blocks from Goldman headquarters in Tribeca. The year-plus since he joined the firm has some in the industry wondering why it has taken Marcus so long to enter the market, but Talwar operates at his own pace. (“Did you hire someone?” his wife of 28 years would ask each night over dinner, last May and June. “Not yet!” he’d reply.) His own recruitment was itself a roundabout process; he declined to return repeated calls about the job, only agreeing to engage after Goldman managing director Sumit Rajpal tracked him down in Washington, D.C., for a brief dinner.

Some hires might have tried to proactively protect against parent-company interference, but not Talwar. “I didn’t agree on any explicit ground rules” about how Marcus would operate, he says, after we order our omelets. “If you have to rely on ground rules, then you need to question. I did my due diligence, but it was on trust, chemistry, commitment.”

In his first weeks on the job, Talwar relied on an internal team on loan from Goldman’s merchant bank and a crew of McKinsey consultants to help him develop a business plan. By Labor Day, he had made nearly a dozen hires, including the merchant bank’s Omer Ismail as his chief operating officer. By around Thanksgiving, when the team wrote its first lines of code, 40 Marcus employees, often dressed in jeans, were attracting side glances in the Goldman elevators.

Team dynamics are central to how Talwar approaches hiring. “In a consumer business there are no rainmakers; it’s not some star trader or star banker or star asset manager,” he says. “It requires a lot of teamwork across different functions.” In interviews, he asks candidates what makes them angry—”that to me reveals their value system.”

Soon Talwar will have to start delivering against the business plan he presented to Goldman’s board of directors. “Everybody understands that in a consumer business you’ve got to invest for some time before you make money,” he says, when asked about the bank’s appetite for burning cash while Marcus gets off the ground. “It’s very clear we are in this for the long run. We will make the investments required to build a business.”

It remains unclear whether that business will have a major impact of Goldman Sachs’s overall fortunes. Like its peers, Goldman has been struggling to maintain a return on equity in the 10% to 12% range that investors have expected of banks. “Unsecured consumer loans have high ROEs,” Talwar says—as high as 20% or more, according to Goldman equity research. Like other retail banking products, their quarterly profits also tend to be more stable than those of trading-based business lines.

Yet Talwar also makes clear, as we settle the bill and finish our coffees, that more is at stake than the usual Wall Street metrics. “We are very much a business of the firm. We will be measured on the revenues, the expenses,” he says. “But as everybody tells me, more importantly we’ll be measured on customer satisfaction.”

“We’re a technology firm”

A lot has happened in the century between Marcus Goldman’s death and today’s launch. For the most part Goldman Sachs thrived, first as an investment bank and later in securities trading and risk arbitrage. But in the early 2000s the financial system began to unravel, along with the bank’s vaunted reputation.

The money-music came to a screeching halt in 2007 to 2009. One pivotal bankruptcy, three major shotgun mergers, three federal takeovers, and over $430 billion in TARP funds later, Wall Street had survived, but barely. In the years since, it has become harder for banks to compete for talent. Average pay per Goldman employee has dropped by 39% (the firm used to offer the best pay on the street). The firm has also cut headcount and implemented a strategy known as “juniorization,” whereby it demotes underperforming partners and eliminates positions left empty by departing managing directors.

“Ten years ago Goldman or one of the large banks would have been viewed as at the top of firms to which our MBA students would love to go,” says Darrell Duffie, a financial economist at the Stanford Graduate School of Business. “Now I would say that’s not as much the case.”

Efforts to rebrand banks as technology-focused innovators have done little to change that narrative. “We’re a technology firm, we’re a platform,” Blankfein asserted on Bloomberg last June, in a rare TV interview.

That may be true insofar as Goldman uses software developed in-house to evaluate risk and manage trades. Indeed, the firm’s SecDB software played a pivotal role in helping Goldman survive the near-implosion of Long-Term Capital Management in 1998 and the housing crisis in 2008. But client-facing software has not been a priority. If Marcus succeeds, it will represent a transformation of the firm’s technology capabilities. Roughly two-thirds of Marcus’s hires have come from outside Goldman, with backgrounds ranging from Lending Club and OnDeck to Etsy and Google.

Back to the future

Marcus arrives at a precarious time for the world’s major banks, Goldman included. Since 2009, more than $100 billion in financial services revenue has gone up in smoke, according to research firm Coalition. While Congress grills Wells Fargo and the Department of Justice lobs fines at Deutsche Bank, a debate is raging in the background over the rules that banks are now required to follow, and whether they are having the desired effect. “Have big banks gotten safer?” former U.S. Secretary of the Treasury Lawrence Summers and Harvard PhD candidate Natasha Sarin ask in a recent working paper. They argue no, based on evidence that it’s now a lot less valuable, by definition, to be a bank. In the meantime, the shadow banking world—from small hedge funds and fintech startups to Silicon Valley giants like Apple and Google—continues to encroach on banking territory.

Goldman, still led by Blankfein at age 62, has been soul-searching amid the turmoil. When the public pounced, eight years ago, other banks did not rush to the firm’s defense. Now, as the overall pie is shrinking, the firm is angling to undercut its competitors’ lucrative credit card businesses. If Marcus succeeds, it will not win Goldman any new Wall Street allies. But it may prove valuable in a variety of other ways: engendering goodwill with regulators, making new friends on Main Street, recasting the bank a more benevolent and tech-savvy employer, and maybe even contributing to Goldman’s bottom line.

Marcus’s achievement of any or all of those goals depends on its ability to convince consumers that it is a new-fangled product with old-fashioned values—in fact, Goldman’s original values, which promised that clients’ interests should always come first. “Good ethics is good business,” former Goldman chairman John Whitehead, who died in 2015, wrote in his memoir. Sometimes, it’s just that simple.

Scherr, chief strategy officer and CEO of GS Bank USA, helped shepherd Marcus from its earliest days as part of a senior task force.

Talwar, a consumer banking veteran, left his post at Discover to start Marcus last spring.

Cohn previously worked for Jockey and PepsiCo; Alfred previously worked for Progressive.

Product team members Nicole Sbarra, Greg Berry, and Carl “Boe” Hartman

Fast Company , Read Full Story

(184)